Why Russian Military Electronics Lag Behind the West

Introduction: A Gap Exposed by War

The 2022-2025 war in Ukraine has served as an unscripted live-fire audit of the Russian defence-industrial base (DIB). The audit exposed the most serious weaknesses in Russian military electronics, mostly optoelectronics and microelectronics. These systems include thermal sights, night-vision devices, radar processors, and guidance chips. They determine which force detects, targets, and strikes first on the modern battlefield. Russian vehicles and munitions often rely on commercial-grade, dual-use, or civilian components. In some cases, investigators found semiconductors taken from household appliances instead of military-grade parts. Ukrainian and Western battlefield-recovery reports have repeatedly documented these substitutions. This gap is not just anecdotal. It can be measured in fabricating nodes, wafer throughput, sensor pixel pitch and import statistics.

Semiconductors: A 15–25 Year Technology Gap

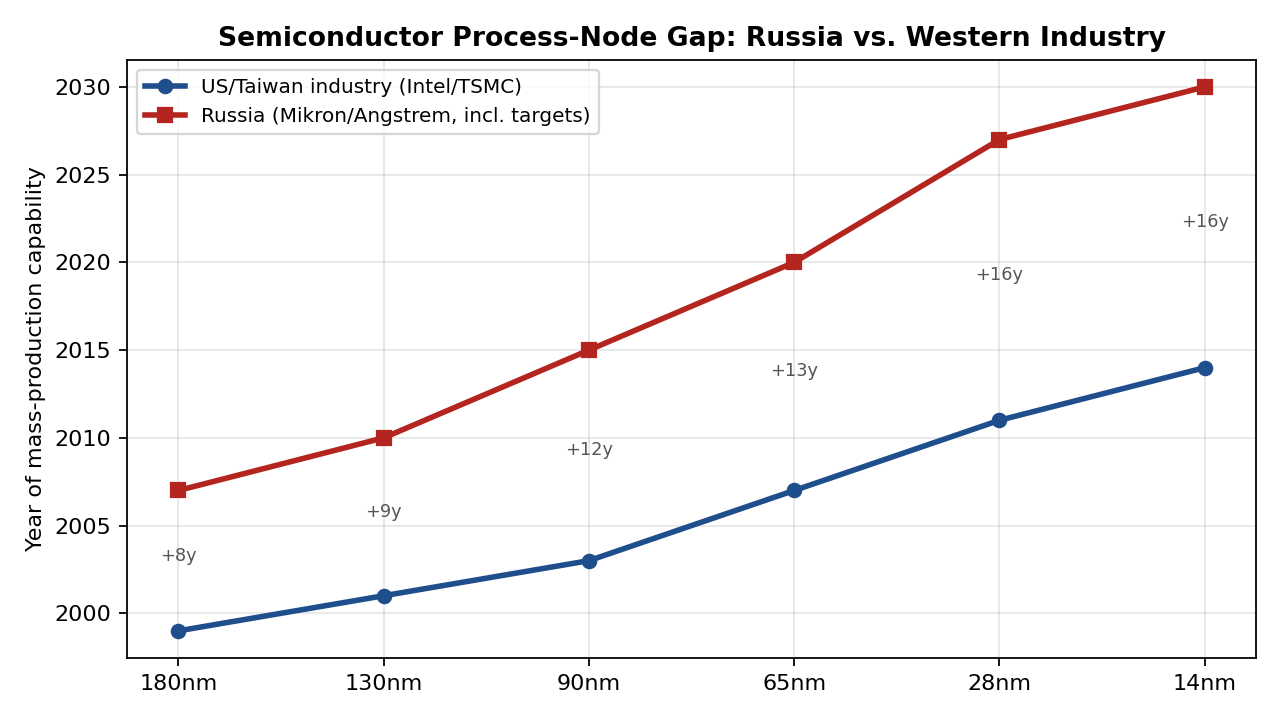

The upstream driver of optronics performance (resolution, frame rate, noise floor, size/weight/power (SWaP)) is semiconductor fabrication capability. Russia’s two largest chip makers, Mikron (Zelenograd) and Angstrem, are structurally unable to compete with Western or Taiwanese process technology. Mikron only got to mass production on the 180nm node in 2007 and claims 65nm qualification since 2020, but independent industry analysts say actual high-volume output is still closer to 90nm since Mikron’s KrF lithography tools cannot reliably support 65nm in volume. The Angstrem range is approximately 250 nm to 90 nm. Intel started 65nm mass production in 2007. TSMC was at 28nm in 2011. Russia is only targeting that node for 2027, not expecting 14nm until 2030.

TSMC or Samsung Support

This situation implies that there is an ongoing 15-25 year interval between successive node generations that is not closing but is arguably widening as Western and Taiwanese foundries continue to advance to sub-3 nm nodes. This scenario strains the capacity of nodes even more. Reported throughput at Mikron is on the order of 6,000 wafers per month, a fraction of a single modern TSMC or Samsung fab line.

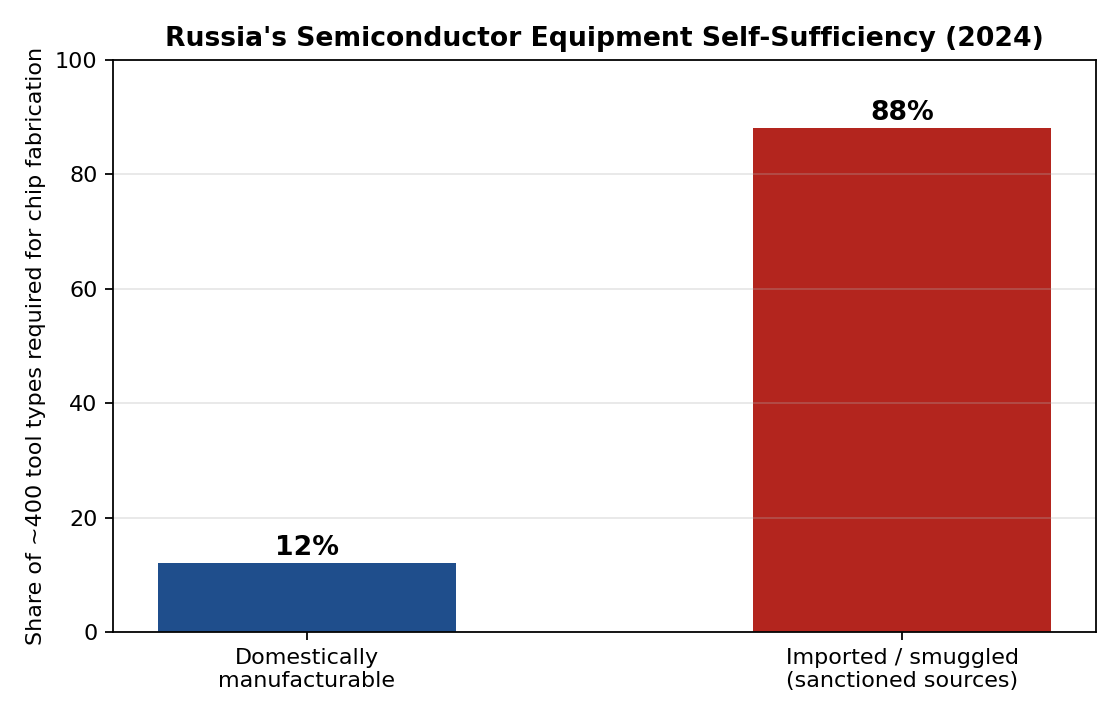

Russia’s technological independence remains limited. Currently, it can supply only 12% of the roughly 400 tool types required for domestic chip production. The rest must be smuggled through third countries or imported at premiums of 40–50% since sanctions began in 2022. In March 2025, the Zelenograd Nanotechnology Centre unveiled Russia’s first domestically produced photolithography tool. It offered 350-nanometre resolution, a process node Western manufacturers abandoned during the late 1990s.

Optronics: The Microbolometer Bottleneck

The thermal imaging sights use microbolometer focal-plane arrays, which are uncooled infrared detector chips that were once the best optronics in Russia and relied on Western technology. Until 2022, high-end Russian thermal sights (series Irbis and Shahin) were heavily dependent on microbolometers from French companies Lynred (ex-Sofradir/ULIS) and Thales. When EU export controls severed that supply chain in 2022, Russian industry – centred on the Shvabe Holding conglomerate within the state defence corporation Rostec – sought to fill the gap with domestic sensor production.

Failure in Production

The results have been inconsistent. Open-source investigators sifting through leaked internal industry communications have suggested that Shvabe has suffered from fabrication yield rates and pixel-to-pixel sensor uniformity issues and has failed to scale production of 12-micron pixel-pitch detectors, the pitch that defines modern high-performance, compact thermal sights (larger pitches like 17-micron or 25-micron produce bulkier, lower-resolution optics for a given lens aperture). The result was seen at the front: mobilised Russian reservists and volunteer units are often armed with mechanical iron sights or Soviet-legacy active-infrared night vision devices (1PN58/1PN93 series) that require an IR illuminator — a design that, unlike passive thermal imaging, actively produces a signature detectable by any enemy with IR-sensitive optics.

A similar case involving the T-14 Armata programme illustrates this dependency. Analysis by Taia Global and The Intercept examined leaked correspondence concerning the programme. It found that Russian industry could not independently produce microbolometer arrays for the tank’s advanced thermal sights. This showed that even flagship weapons platforms remained vulnerable to foreign component dependence.

Sanctions: Measuring the Impact

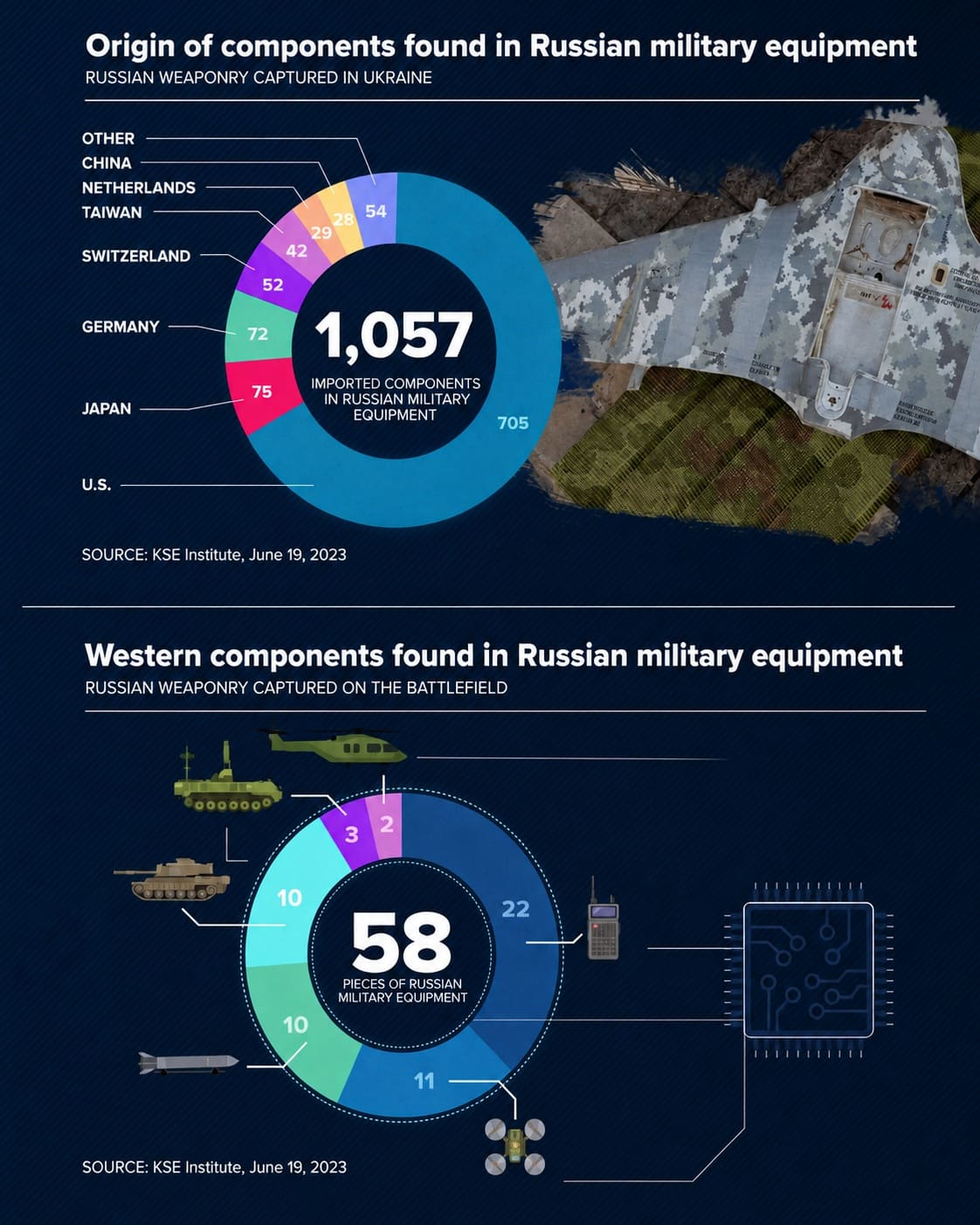

In June 2022, U.S. Commerce Secretary Gina Raimondo said that global semiconductor exports to Russia had fallen by about 90% after coordinated actions by the U.S. and allied governments to limit those exports. In 2022, the Russian army also lacked night vision and thermal imaging equipment and could not outfit standard infantry loadouts with that alone. According to research by the American Enterprise Institute, roughly 88% of Russia’s semiconductor purchases in the first half of 2023 came from chips made in China. This move represents a wholesale shift of dependency from the West to China, but it does not address the underlying dependency.

Structural and Historical Causes

Three structural factors explain why Russia has not closed this gap despite two decades of stated intent:

(a) Absence of a civilian commercial semiconductor ecosystem. Massive civilian markets – smartphones, automotive, and consumer electronics – indirectly subsidise Western and Taiwanese dominance in optronics-relevant chips (CMOS image sensors, FPGAs, and DSPs), which fund the capital expenditure (a single leading-edge fab now costs $15–$20 billion) that is later amortised into defence applications. Russia’s demand for chips is primarily military and state-payment-system driven (Mikron’s chips support the domestic Mir card network), creating a market too small to justify similar capital investment.

(b) Post-Soviet disinvestment and brain drain. By the 1980s, the Soviet optoelectronics and microelectronics complex in Zelenograd had become internationally competitive. However, it suffered catastrophic underinvestment after the Soviet Union collapsed in 1991. The departure of skilled engineers for Western and Israeli firms accelerated the sector’s decline. Some companies, including Sofradir’s precursor entities, later became suppliers on which Russia depended.

(c) Sanctions-driven tooling isolation. A handful of Western and Japanese companies (ASML, Applied Materials, Tokyo Electron, and KLA) dominate the lithography, deposition, and metrology tools. But node capability is gated by tool capability, and export controls on these tools, not finished chips, cap Russia’s ceiling, no matter how much domestic design talent it has.

Adaptation and Future Outlook

Russia’s primary adaptive approach has been to outsource to China’s commercial optics industry, which is based in Wuhan’s “Optics Valley” and Yantai and has built a sizeable thermal-imaging manufacturing base over the past decade. This industry now offers “commercial-grade” units that are good enough, if not as good as Western mil-spec performance, to satisfy Russian battlefield demand. On the domestic front, Russia’s stated targets remain unchanged: 28nm by 2027, 14nm by 2030, and 70% equipment localisation by 2030. But independent assessments like that of the American Enterprise Institute suggest that these goals are unlikely to be met on time due to the cumulative effect of sanctions, capital constraints and the moving target of Western technological advancement.

Conclusion

The Russian gap in optronics and electronics is not a one-off failure but a layered one: a backward fabrication base fifteen to twenty-five years behind the technological frontier; a critical sensor bottleneck in microbolometer manufacturing; an equipment-tooling dependency that sanctions have deliberately targeted; and structural economic conditions that make organic closure of the gap improbable within the next decade. “Substitution through Chinese supply chains has been reduced but has not eliminated dependence; it has merely shifted it.

References

- Carnegie Endowment for International Peace. (2024, March). This article examines why Russia has been so resilient to Western export controls. https://carnegieendowment.org/russia-eurasia/research/2024/03/why-russia-has-been-so-resilient-to-western-export-controls

- Frontelligence Insight. (2025, May 19). Through the optics of war: How Shvabe and Rostec are modernising under sanctions. https://frontelligence.substack.com/p/through-the-optics-of-war-how-shvabe

- Alperovitch Institute / Ronin’s Grips. (2025, November 28). How Chinese optics are transforming Russian warfare. https://blog.roninsgrips.com/how-chinese-optics-are-transforming-russian-warfare/

- Tom’s Hardware. (2024, October 14). Russia to spend $2.5 billion on domestic chipmaking tool tech [republished via Evertiq]. https://evertiq.com/news/56560