SAP Defense Push Reshapes AI and Revenue Risk

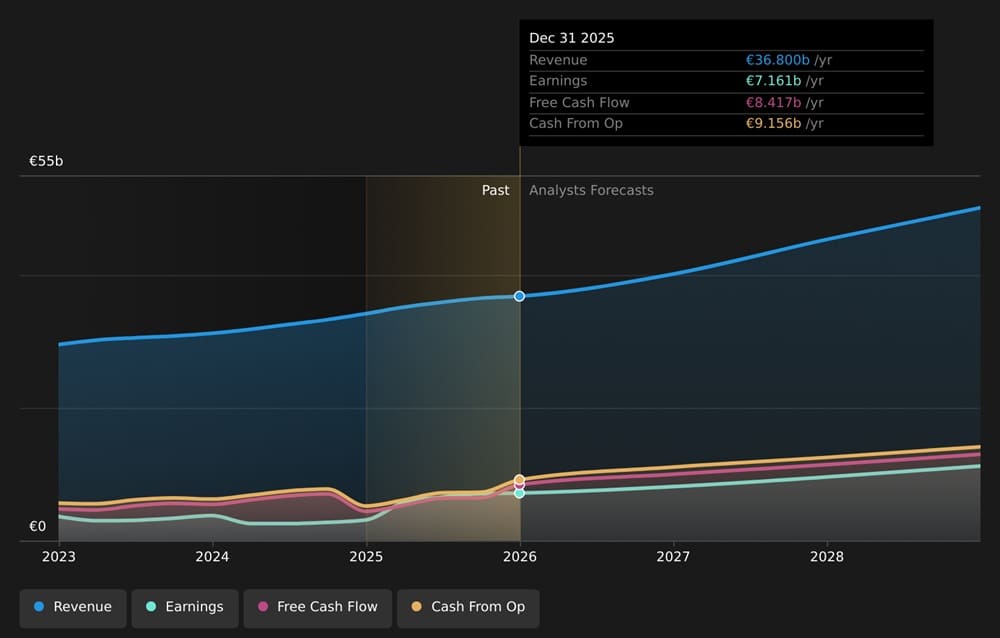

It seems that SAP is currently experiencing a significant strategic shift. SAP Investor Relations listed the share at €160.12 on March 19, 2026, so the valuation snapshot below should be regarded as time-specific. The long view is still impressive. Over three years, the shares have increased by 40.2%, and over five years, they have increased by 62.3%. The shorter image is weaker, though. The stock has dropped 38.4% in a year, 23.8% so far, 7.6% in the last seven days, and 11.3% in the last thirty days. Because investors are no longer pricing SAP as merely a cloud transition story, this split is significant.

Why SAP’s Defense Push Matters

The SAP defense push is now much more important to the investment case. Christian Klein, the CEO, said this week that defense is SAP’s fastest-growing business line and makes up about 10% of the company’s total revenue. SAP has also made the direction clearer by opening a defense innovation hub in Munich and by actively promoting specialized defense and security software for use on land, sea, air, space, and the internet.

That change is in line with SAP’s bigger plan. Customers in the defense industry typically purchase systems that are challenging to replace once established. They need money, transportation, asset management, procurement control, visibility into their workforce, and safe data handling. So, the SAP defense push could make recurring revenue stronger, contracts last longer, and switching costs higher. SAP’s own industry materials describe these tools as mission-ready software instead of just back-office products.

Why Investors Like This Mix

For bullish investors, the most important thing is the quality of the revenue, not the excitement. Mission-critical software usually stays in place for a long time. When an armed force, ministry, or defense contractor builds planning and maintenance workflows around a platform, it becomes costly and time-consuming to replace it. That can help with regular updates and follow-up work, especially when cloud services, analytics, and AI tools are added on top of the original ERP layer.

SAP is also trying to tie this defense opportunity into its main AI story instead of treating it as a separate consulting opportunity. In January, Reuters said that SAP Business AI was part of two-thirds of cloud order entry in the fourth quarter. SAP’s partnership with LatticeFlow also provides technical assessments and governance tools for AI apps that run on SAP AI Core. That’s important because defense buyers don’t just want algorithms. They want to be able to track things, test them, control risks, and audit them.

How the Risk Profile Changes

The same trend also brings up new points of pressure. Defense spending is often difficult to change, but it is never politically neutral. Election cycles, budget reviews, export controls, sanctions, procurement rules, and changing alliance priorities can all have an effect on contracts. Because of this, investors shouldn’t think that every euro of defense software revenue should receive the same valuation multiple as a regular commercial cloud subscription.

There is also the risk of execution. Deployments for defense are usually difficult. Old databases, classified environments, disconnected operations, sovereign hosting needs, and lengthy approval chains are some examples of these risks. Even big software companies can see their profits drop when projects become too customized or too reliant on public-sector deadlines. Investors should closely monitor whether SAP’s defense wins remain anchored in standard cloud ERP, supply chain, and data governance products, or if they shift towards one-off program work.

AI makes things even more sensitive. The EU AI Act went into effect on August 1, 2024. Most of its rules will take effect on August 2, 2026, but some are already in effect. That doesn’t stop SAP from reaching its goals. But it does mean that accountability, governance, model testing, and documentation will be more important. This challenge is now a compliance issue as well as a valuation issue for a company that wants AI to be a part of important public workflows.

Why the Market Stays Cautious

Recent changes in the stock price show that investors are quick to punish SAP when they lose faith. Reuters said that SAP shares had their biggest one-day drop since 2020 after the company’s January results did not ease worries about the cloud backlog and the cloud outlook for 2026. This news is important for the SAP defense push because the market still wants to see proof that new themes help the core engine instead of getting in the way of it.

Investors may see defense growth as a mixed blessing if it means slower cloud growth, less transparency, or higher delivery costs. On the other hand, if SAP can show that defense demand pulls through its current cloud suite, improves the quality of its backlog, and makes it easier to see when contracts are up for renewal, the story changes. Then the SAP defense push stops looking like a side bet and starts to look like a long-term addition to SAP’s software base.

What to watch next

Investors should focus on three key areas. First, see if SAP provides additional information about defense-related sales, types of customers, and contract margins. Secondly, monitor whether management continues to associate defense wins with standardized cloud and AI products, rather than custom services. Third, pay attention to governance. In this area, new contract announcements may not be as important as progress on AI assurance, risk controls, and regulatory alignment.

For related context on how military users are absorbing digital tools, see Defense News Today’s coverage of US AI Tools in Iran War: What CENTCOM Confirmed and How the GBU-57 MOP Bunker Buster Works. On the external side, SAP’s AI GO! for SAP AI Core with LatticeFlow and the European Commission’s AI Act framework page are worth following.

The SAP defense push makes the growth story stronger and more complicated at the same time. The chance is real because defense buyers need software that is strong and well-integrated, and they want AI that comes with rules. However, the revenue will only be worth a lot if SAP stays focused on its core strengths in ERP, cloud platforms, data control, and compliance. If it does, defense could become a long-term advantage. Investors may witness a software leader relocate to a more volatile region if it doesn’t.

References

- https://www.sap.com/investors/en/stock.html

- https://www.reuters.com/business/sap-meets-q4-revenue-forecasts-cloud-demand-holds-up-2026-01-29/

- https://news.sap.com/2026/02/sap-launches-defense-innovation-hub-digital-resilience-strategy-readiness/

- https://digital-strategy.ec.europa.eu/en/policies/regulatory-framework-ai